Why do I need Shareholder Protection?

Without Shareholder Protection cover, if something happens to one of the

shareholders in your company, you may have no choice who you end up being in

business with... for example:

- your business partner's wife

- your business partner's lawyer or accountant

- your business partner's wife's brother

When do I need Shareholder Protection?

It's worthwhile considering Shareholder Protection cover if there is more

than one shareholder and your company has a dollar value. Essentially,

if you cannot afford to 'buy out' a shareholders shares immediately, you

need to consider Shareholder Protection cover.

When is Shareholder Protection not required?

If you are a sole trader (i.e. you have no shareholders) or if you run your business with your spouse. In both cases, if something were to happen to you, your shares would go to your estate.

If you have a relatively new company or your company has no capital value, then you don't require Shareholder Protection just yet... but it is worth understanding how it works so that you can determine when you need to consider cover in the future.

What is a Buy/Sell Agreement?

It is important to review your current buy/sell agreement or put one in place when you take out Shareholder Protection cover as it sets out the ground rules of what happens if a shareholder dies or is taken out of the business. It specifies when the shares need to be sold, who will purchase them and in what timeframe.

A buy/sell agreement is just as important as the insurance... one without the other is useless.

Case studies

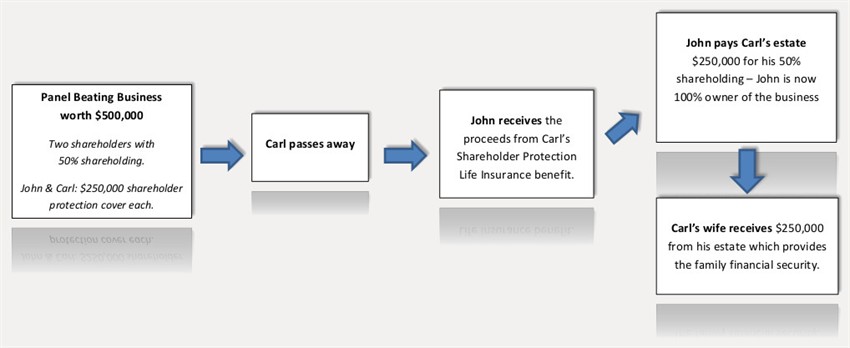

Case Study 1:

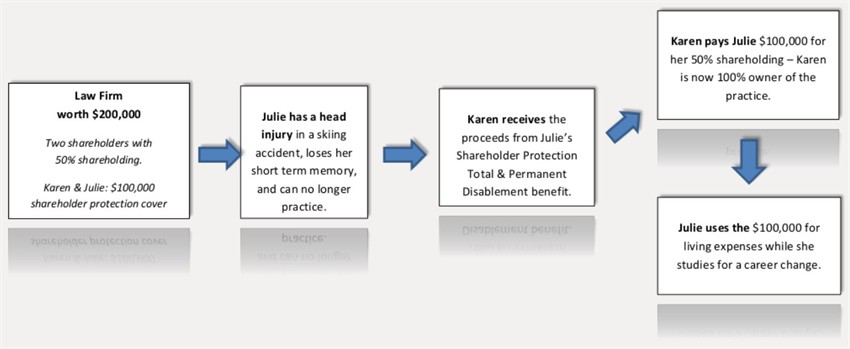

Case Study 2:

Take action

Talk to us about the life you want, and how to make sure it happens, no matter what.